Financial Tips

According to our experience in dealership business and plenty of finance sales we have made, we would like to give you some tips before you go finance a vehicle.

The Quality:

When you buy any used vehicle, you have to keep quality as a priority along with the price in order to have a vehicle that will last without any problem till the end of the loan term and after.

Many walk-in customers shop for a vehicle like they shop for a pack of cigarettes. They go from dealer to dealer with a pen and paper writing down the price, year, and mileage without even listening to the vehicle running. Please take the chance to look underneath the vehicle and know who you are dealing with. Many bad dealers are there and many vehicles appear very nice and shiny on the outside but you will be surprised if you take a look underneath. Click here to see some pictures as an example.

The Annual Mileage:

You have to keep your eyes open on the mileage of the vehicle that you are going to finance along with how many miles you will put on the vehicle every year.

For Example: Don't finance a vehicle that already has 150K miles for 48 months loan term if you put 50K mile/year on the car because by calculation the vehicle will have 350K miles by the time you are finished with your payments, before that the car will need major repairs (cost more than what it is worth) or it will be broken down. I see many customers who have broken down cars and they are still engaged in payments. Most of these customers get repossession and it will be hard for them to get a loan for another car with a decent interest rate.

So don't stretch the term of the loan to meet your monthly affordable payment without the consideration of your yearly mileage.

Also, keep in mind that when you finance a low mileage vehicle, you will have a good chance to resell it or trade it in when you would like to switch to a new vehicle.

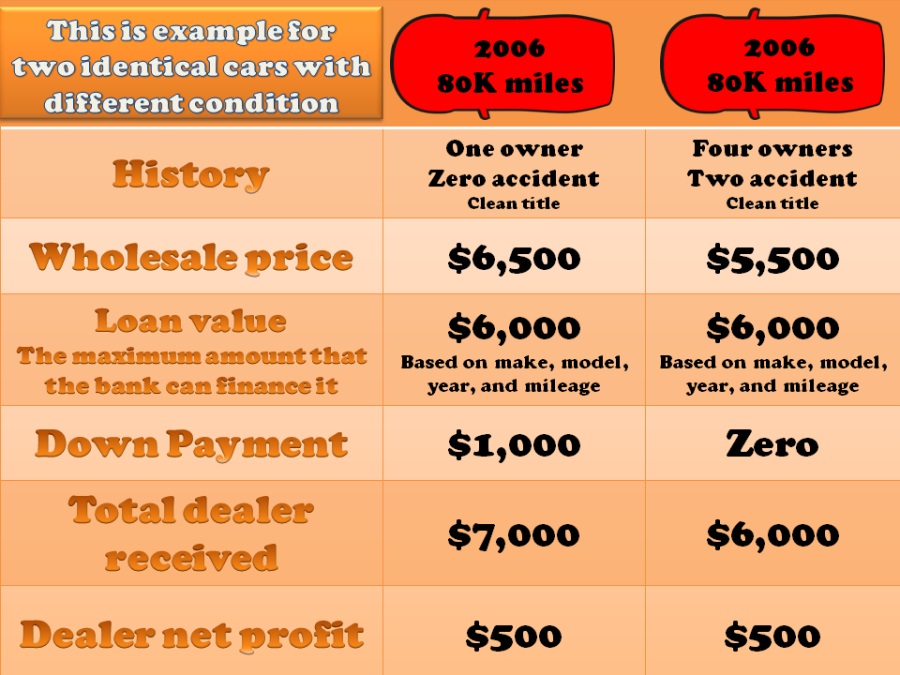

Down Payment vs. Loan Value:

Don't make the wrong decision by going to very low down payment deal to finance a vehicle. Every vehicle has "Loan value" same as "Retail value" and "Trade in value".

The loan amount of any vehicle is determined by the bank/lender base on the year, make, model, and mileage regardless the condition of the vehicle. The bank/lender don't check the vehicle. It is your duty to check the vehicle.

Absolutely, the difference between the selling price and the loan value is the down payment that you should pay in front plus tax, etc. If a dealer advertises or accepts very low down payment, that means he bought it very cheap due to the condition of the vehicle. "Don't make the wrong decision"

Additional Services:

By law, you have the choice to add any additional services to your loan no matter what the dealer says to you. Please give yourself time to read the "Retail Installment Contract" before you sign it. Keep in mind that NO ADDITIONAL SERVICE IS MANDATORY and you have to sign Disclosure and Agreement for any additional service.

Additional service such as:

VSC: Vehicle Service Contract (Warranty). More options could be better and cheaper.

GAP Insurance: Guarantee Asset Protection (preferred).

GPS / SID: Vehicle Starter Interruption Device and GPS System. (not recommended)

GAP insurance:

Guaranteed Asset Protection. Gap insurance covers the difference (or gap) between what the car is worth and what you owe on the car. It comes into play if your car is stolen or totaled while you are still making payments. This GAP covers the difference between the actual cash value of the vehicle and the balance still owed to the lender. When you choose to purchase GAP Insurance, that gives you the opportunity to pay less down payment because the lender protects his borrowed money the same as you protect your asset.

Protect Your Investment:

In order to avoid any risk or loss, it is a smart decision to purchase a VSC "Vehicle Service Contract". Now, you can purchase VSC as you go (month by month). It cost you $39.95 per month. That is less than a cost of a cup of coffee a day. You can participate for three or six months. Once you ensure that the vehicle is running fine, you can terminate it. If you would like to continue, that will be much better.

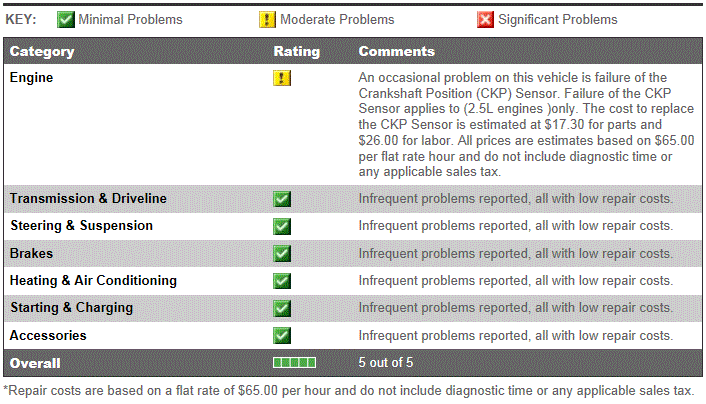

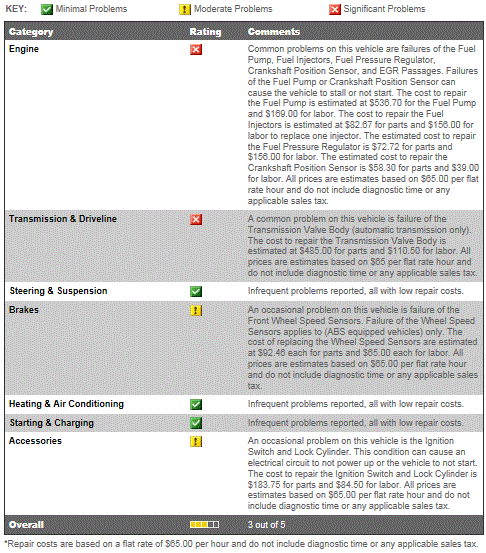

The Reliability Rating:

Most of the cars on the market are known for failure problems. I advise any customer especially the ones who have a tight budget to do their homework before you select the car they are going to finance. Check the reliability rating or read some reviews of the vehicle that you are going to finance.

Keep your eyes open on the repair cost for the known problems. As I mentioned most of the vehicles have a failure problem but which is major and which is simple; which is common and which is occasional.

For Example, Car is known for the failure of the knock sensor. The part costs $26 and the repair cost is $65. I can deal with that.

A car is known for a bad transmission. The part costs $1,000 and the labor cost is $450. I should stay away from this vehicle.

Example for good (reliable) vehicle:

Example for bad (unreliable) vehicle:

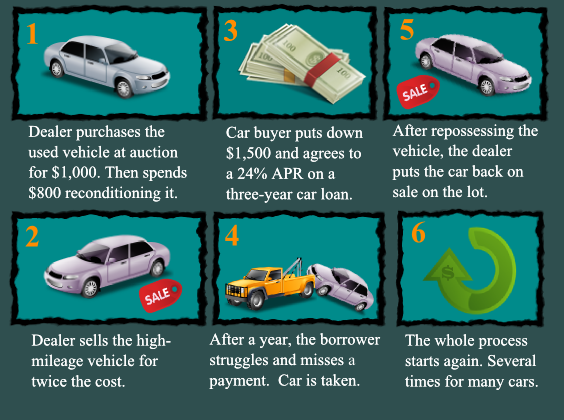

How Buy Here Pay Here works:

The image below explains how BHPH works. Also, they don't report to any of credit bureau. If you need to rebuild your credit or establish credit, BHPH is not the right choice.

The Maintenance:

The car cost is not just the monthly payment. It is gas, repair, and parts. Before you decide to finance the car, think about these items to keep your vehicle in good running condition along with making your payment affordable.

The Budget:

If you have a tight budget, pick the vehicle that gets you more usage with less cost. For example; if you have to choose (with same monthly payment) between a 2008 vehicle with 145K mile and 2002 same make and model with 65K mile, go with 2002 with low mileage because it will serve you better and you will get an extra 80K mile of usage.

The Need:

Before you finance a vehicle, think "Do I want it? OR Do I need it?". Finance the vehicle that meets your needs and your affordability. For example, don't finance a truck for a high monthly payment and use it as a car because you like to drive a truck.